The LMS provider Docebo commissioned a fantastic report on the health of the elearning industry. It is a document that I have referred to a great deal in recent months, so thought I would share the facts and figures that I found most useful/interesting. All content is taken directly from the Docebo report. A link to the full document can be found at the end of this post.

Trends and forecast in eLearning

There seems to be universal agreement that the worldwide E-Learning market will show fast and significant growth over the next three years. The worldwide market for Self-Paced E-Learning reached $35.6 billion in 2011. The five-year compound annual growth rate is estimated at around 7.6% so revenues should reach some $51.5 billion by 2016. While the aggregate growth rate is 7.6%, several world regions appear to have significantly higher growth rates. According to recent regional studies, the highest growth rate is in Asia at 17.3%, followed by Eastern Europe, Africa, and Latin America at 16.9%, 15.2%, and 14.6%, respectively.

Each of the world’s regions has its idiosyncrasies In terms of the factors that drive this market. The U.S. and Western Europe markets are the most mature. The U.S.A. spent more on Self-Paced E-Learning than anywhere else in the world.

Western Europe is the world’s second largest buying region for E-Learning products and services but Asia is predicted to outspend Western Europe in E-Learning terms by 2016.

In 2012, Bersin & Associates stated that there were some 500 providers in the LMS market and only five of them have more than a 4% market share. According to this, the LMS market was expected to reach $1.9 billion in 2013. However the growth exceeded expectations, closing the year at $2.55 billion.

E-Learning is subjected to the influences of sales trends related to smart connected devices and the Internet megatrend (that is, the spread of the Internet in the world).

According to IDC, the number of PCs will fall from 28.7% of the device market in 2013 to 13% in 2017. Tablets will increase from 11.8% in 2013 to 16.5% by 2017, and smartphones will increase from 59.5% to 70.5%.

The new frontier to address is the trend towards Bring Your Own Device (BYOD) — where individuals take their personal (usually mobile) devices to workplaces. Increasingly, these seem to be being used to help their owners perform work activities (including formal training), both in and out of the workplace. Smartphones are the most common examples of these devices but employees often also use their tablets or laptops in the workplace.

While the corporate-training market has lagged behind other education-based sectors, it continues to represent a viable investment opportunity. The corporate-training market is among the most cyclical within the education industry. Since 2010, employers’ total spending on training and the amount spent per employee — the key data used to measure this sector — have been

declining. However, the corporate market related to outsourced services (net of all ancillary costs) has grown to reach 42% of total expenditure.

Within the training industry, the E-Learning sector has grown consistently in recent years. All its subsectors (Packaged Content, Platform, and Authoring tools) show positive annual

growth. Market acceptance of E-Learning has resulted in its increased use for both large and small companies. SaaS/ Cloud E-Learning solutions are particularly suitable for Organizations ranging from SMEs to large institutions.

General budget constraints appear to be the main drivers of the shift towards using E-Learning. However, E-Learning is not merely a solution which is attractive during an economic downturn but it is also an efficient and cost-effective solution when workers — especially those in Organizations with a widely geographically distributed workforce — need to be brought up-to-speed quickly on relevant knowledge and skills.

With the inflow of an estimated $6 billion of venture capital over the past five years, E-Learning is being driven not only by startup dot-com entrepreneurs but also by big corporations, for-profit spin-off ventures, as well as big and small universities.

According to Product & Users, the LMS market is expected to experience a growth of 23.17% between 2017 and 2018. According to Ambient Insight, the packaged content market will reach $38.3 billion by 2016 (SOURCE: AMBIENT INSIGHT 2012).

According to sources, large and affirmed Companies (such as the Global 5000) are the primary buyers of E-Learning products and services. They account for more than 30% of the E-Learning Market clientele.

Total E-Learning Market

(LMS + Packaged Content + Other Services)

|

2013 |

2016 |

| Total |

40.605 |

51.172 |

| North America |

23.800 |

27.100 |

| Western Europe |

6.800 |

8.100 |

| Eastern Europe |

729 |

1.200 |

| Asia |

7.100 |

11.500 |

| Middle East |

443 |

560 |

| Africa |

333 |

512 |

| Latin America |

1.400 |

2.200 |

Packaged Content

|

2013 |

2016 |

| Total |

30.153 |

38.000 |

| North America |

17.674 |

20.124 |

| Western Europe |

5.050 |

6.015 |

| Eastern Europe |

541 |

891 |

| Asia |

5.272 |

8.540 |

| Middle East |

329 |

416 |

| Africa |

247 |

380 |

| Latin America |

1.040 |

1.634 |

LMS Market

(covering all the technical solutions available)

|

2013 |

2016 |

| Total |

2.550 |

3.214 |

| North America |

1.495 |

1.702 |

| Western Europe |

427 |

509 |

| Eastern Europe |

46 |

75 |

| Asia |

446 |

722 |

| Middle East |

28 |

35 |

| Africa |

21 |

32 |

| Latin America |

88 |

138 |

Other services related to E-Learning activities

|

2013 |

2016 |

| Total |

7.902 |

9.958 |

| North America |

4.632 |

5.274 |

| Western Europe |

1.323 |

1.576 |

| Eastern Europe |

142 |

234 |

| Asia |

1.382 |

2.238 |

| Middle East |

86 |

109 |

| Africa |

65 |

100 |

| Latin America |

272 |

428 |

AFRICA

The people of Africa seem willing to engage with new technologically-based tools to improve their education, knowledge and skills. However, the continent’s infrastructure is proving to be a major challenge and an obstacle to meeting this growing level of demand.

| 2013 Revenues |

$332.9M |

| Annual growth rate |

15.2% |

| Revenues by 2016 |

$512.7M |

EASTERN EUROPE

| 2013 Revenues |

$728.8M |

| Annual growth rate |

16.9% |

| Revenues by 2016 |

$1.2B |

ASIA

Asia has the world’s highest regional growth rate for E-Learning, of 17.3%.

Revenues from the sale of E-Learning reached $5.2 billion in 2011 and are expected to more than double to $11.5 billion by 2016. The vast majority of these revenues will be generated from the sales of packaged content.

| 2013 Revenues |

$7.1B |

| Annual growth rate |

17.3% |

| Revenues by 2016 |

$11.5B |

NORTH AMERICA

North America is the most mature market for E-Learning in the world. In 2011, the U.S.A. spent more on Self-Paced E-Learning than anywhere else in the world.

While the rate of growth in this market may seem low compared with other world regions (at a mere 4.4%), the revenues generated in this market are extremely high.

| 2013 Revenues |

$23.8B |

| Annual growth rate |

4.4% |

| Revenues by 2016 |

$27.1B |

WESTERN EUROPE

Western Europe is the world’s second largest buying region for E-Learning products and services after North America.

This is set to change in the upcoming forecasted period. Asia is predicted to outspend Western Europe in E-Learning terms by 2016.

“Despite being a mature market, 2013 was nevertheless a transitional year for E-Learning in Western Europe. We can put aside the buzz about MOOCs in higher education and all the noise about a coming shift to mobile.

“For those of us who focus on workplace learning, the interesting shift is the number of small and medium sized businesses that have started to adopt sophisticated learning technologies. With the pricing structure of products such as Docebo, suddenly smaller companies are realizing that there is a very low barrier to entry for them to have enterprise grade capability in this area.

“The other trend we’ve observed, from the larger corporations in our client base, is a shift to outsourcing the development of E-Learning content to professional agencies rather than building in-house. We’re excited about the landscape for 2014.”

Guy McEvoy, Managing Director, Guykat

| 2013 Revenues |

$6.8B |

| Annual growth rate |

5.8% |

| Revenues by 2016 |

$8.1B |

LATIN AMERICA

| 2013 Revenues |

$1.4B |

| Annual growth rate |

14.6% |

| Revenues by 2016 |

$2.2B |

MIDDLE EAST

The Middle Eastern E-Learning market is growing rapidly due to market makers, such as Governments, Private Schools and Corporations. This infographic relates to 2013 E-Learning revenues, the market annual growth rate and the forecasts for revenues in 2016.

Oman is the top performer in E-Learning terms for the rankings that cover the Middle East. Oman has the highest growth rate in the region at 19.6%, followed by Lebanon (16.0%), Turkey (12.9%), Kuwait (12.6%) and Qatar (11.3%).

This is mainly because the Government of Oman is interested in issues relating to education and computer literacy and, consequently, is investing heavily in the sector.

For example, Sultan Qaboos University (SQU) regularly provides professional development workshops for its staff.

This acquaints them with E-Learning technology from an educator’s perspective. To date, over 200 staff have attended such workshops. In addition, almost as many regular courses have some E-Learning content included.

“Middle Eastern Governments are strongly committed to promoting a Mass Digitalization process. This means that heavy investments are being made in this initiative. This is especially true for Soft Skills training. This is designed to quickly and competitively improve the workforce. Is compliance training in this region the next “big thing”? Time will tell, but lots of regulations are already coming…”

Claudio Erba, CEO & Founder, Docebo

| 2013 Revenues |

$443m |

| Annual growth rate |

8.2% |

| Revenues by 2016 |

$560.7M |

All content is copyright © 2014 Docebo – All rights reserved.

The full report can be downloaded from the Docebo website at:

https://www.docebo.com/landing/contactform/elearning-market-trends-and-forecast-2014-2016-docebo-report.pdf

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

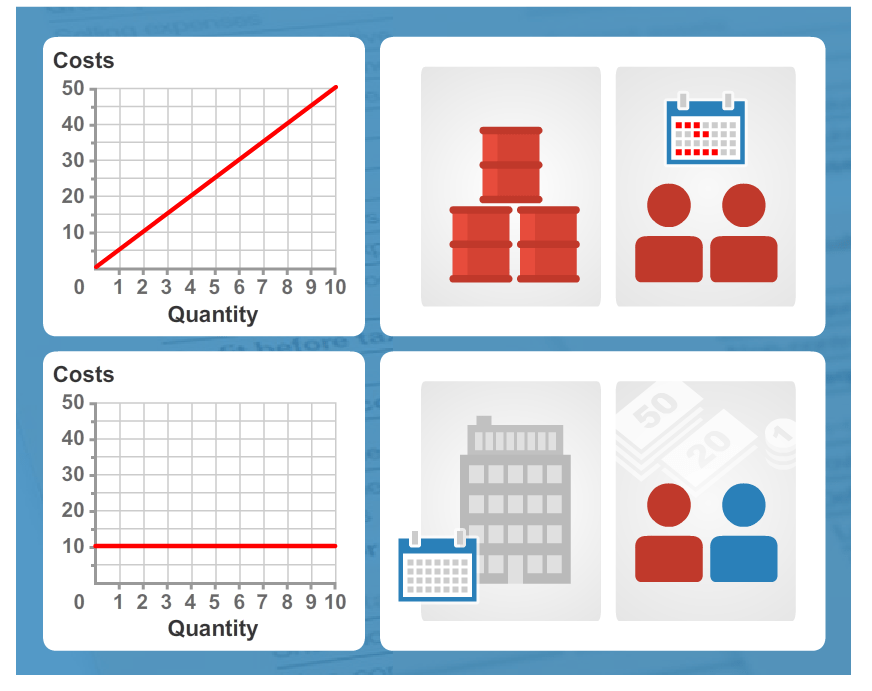

Unlike some materials costs, labour costs represent an immediate cash flow out of a company. Most businesses account differently for direct labour costs (e.g. people directly involved in producing a product) and indirect labour costs.

Unlike some materials costs, labour costs represent an immediate cash flow out of a company. Most businesses account differently for direct labour costs (e.g. people directly involved in producing a product) and indirect labour costs.

{kind=link}