A short guide to the Profit and Loss Account (P&L) for Non-Financial Managers…

A short guide to the Profit and Loss Account (P&L) for Non-Financial Managers…

The P&L (also known as the Income Statement) is a Financial Statement that records the level of profit – or loss – that a business earns over a defined period of time (usually one year).

It does this by relating the income (also known as ‘sales’ or ‘revenues’) the business has earned to the costs and expenses the business has incurred.

The P&L starts by recording the income a company has generated through its sales over a given period. It then deducts a series of costs and expenses from this total to determine several different profit measures.

Cost of Sales is deducted from Sales to produce Gross Profit. ‘Cost of Sales’ are those outgoings which are most closely linked with providing services to clients, buying goods for re-sale, or manufacturing products.

Expenses are deducted from Gross Profit to produce Operating Profit or EBIT (Earnings Before Interest and Tax). ‘Expenses’ are incurred in the course of running the business on a day-to-day basis (e.g. advertising costs). They are not directly linked to sales.

Tax on profits and interest on borrowings are deducted from Operating Profit to produce Net Profit After Tax (or NPAT).

Dividends owed to the business’ shareholders are taken away from NPAT, resulting in Retained Profit.

Retained Profit is the proportion of sales/income that the company keeps, and can then use to drive further growth and investment. In this way, it is the ‘wealth’ the company has produced.

Sales may be made – and inputs may be supplied – on credit. This means that cash transactions for both sales and costs may not happen during the financial period.

So measuring profits requires accountants to analyse a company’s operating performance over a given period, by calculating costs incurred and sales made. This must be done accurately, despite the fact that associated cash flows may occur in different time periods.

Costs can only be entered onto the P&L if they relate to business activities that occurred during the period in question.

Materials are only counted if they were ‘consumed’ (otherwise they are counted as ‘stock’ – which is an asset, not a cost).

Services and overheads (e.g. power) are counted when bought (irrespective of cash flows).

Companies will pay interest on short-term bank loans and long-term financing from a variety of sources. Businesses will also receive interest payments on any investments they hold, plus their bank accounts.

The amount of tax owed on a business’ profits is calculated after interest has been deducted. Actual tax paid may be deferred into the future – but what is called a ‘provision’ is made in the P&L at this point to cover that payment, and counted as a deduction.

The level of dividends paid is decided by the business’ Directors. They will consider both the company’s projected cash needs, and what shareholders expect.

Profit & Loss Account – Costs

A business works out how much material it has actually used over the course of a given financial period with the following equation:

Opening stock + Purchases – Closing stock = Materials used.

Usually, materials are valued on the basis of ‘historical cost’ (e.g. what the company paid for them at time of purchase).

Unlike some materials costs, labour costs represent an immediate cash flow out of a company. Most businesses account differently for direct labour costs (e.g. people directly involved in producing a product) and indirect labour costs.

Unlike some materials costs, labour costs represent an immediate cash flow out of a company. Most businesses account differently for direct labour costs (e.g. people directly involved in producing a product) and indirect labour costs.

Depreciation is an accounting method used to spread the cost of capital assets in use for the long-term over the expected length of their ‘useful lifetime’. A depreciation expense is thus charged to the P&L for every year of that ‘asset lifetime’. So if machine costs 100 and is expected to last for 10 years, an annual depreciation charge of 10 (for example) could be charged for every year.

Depreciation is an accounting method used to spread the cost of capital assets in use for the long-term over the expected length of their ‘useful lifetime’. A depreciation expense is thus charged to the P&L for every year of that ‘asset lifetime’. So if machine costs 100 and is expected to last for 10 years, an annual depreciation charge of 10 (for example) could be charged for every year.

There are different ways of classifying the remaining costs that must be accounted for on a P&L. Most companies divide these according to business function e.g. admin, R&D, manufacturing, sales or advertising.

There are different ways of classifying the remaining costs that must be accounted for on a P&L. Most companies divide these according to business function e.g. admin, R&D, manufacturing, sales or advertising.

Including a cost in the P&L is based on whether it has been consumed during the period in question – irrespective of any cash flows out of the company. But this works the other way too: so if something has been paid for in advance, it will not be accounted for on the P&L until the financial period during which it is used.

Sometimes a business will use things that it hasn’t yet been charged for. In such situations (e.g. water used but not yet billed for) the company must make an estimate of the cost, and include that on the P&L.

Some potential (but likely) costs may need to be accounted for on the P&L in the form of provisions: but for these costs, the full details are not yet clear. For example, an on-going court case may result in a future financial liability (e.g. a fine). Here, the exercise of judgement is crucial on a ‘prudent’ basis (e.g. the business should recognise such issues as soon as they become likely).

A business will spend money on some costs (e.g. training) which can properly be counted as ‘intangible investments’ that will benefit it in the future. However, prudence dictates that their costs should still be recognised in the period in which they are incurred.

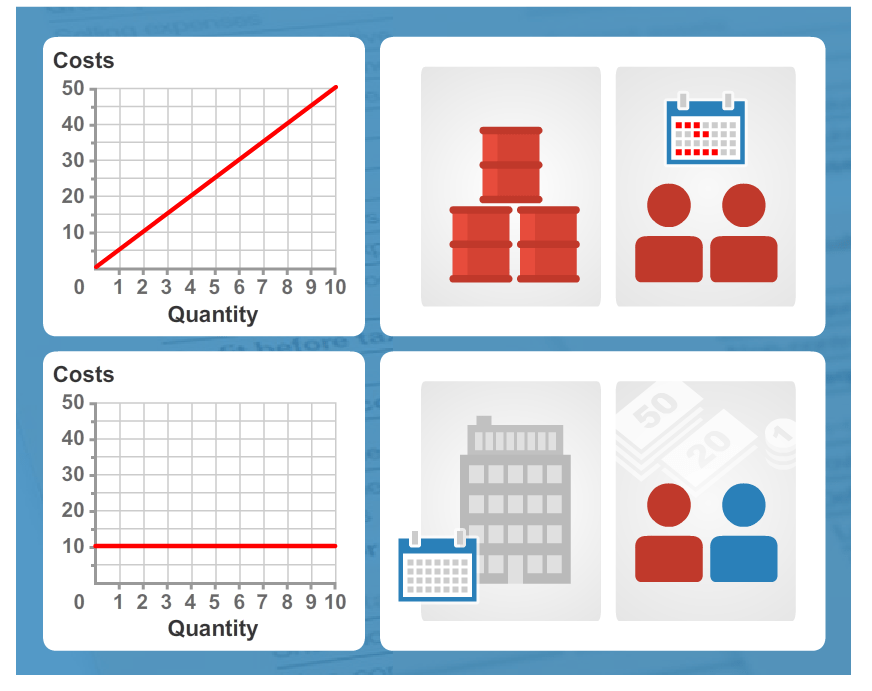

Variable costs are those costs and expenses which change in direct proportion to the level of output (or other business activities). Examples of variable costs include: Temporary labour and materials required to manufacture products; Buying goods for resale; Some selling and admin costs.

Fixed costs are those costs and expenses that usually stay at the same level whatever the level of business activity is (at least over the short term). Examples of these types of costs include office rent and regular salaries.

Breaking down costs into fixed and variable elements allows businesses to identify the marginal costs involved with making extra goods and products more clearly. This is known as ‘variable costing’.

About Brightbolts…

Brightbolts supports business by raising the financial literacy and business acumen of managers.

Brightbolts are specialists in helping managers and organisations raise their levels of financial literacy and commercial awareness. Our suite of customisable Finance for Non-Financial Managers eLearning courses are used by leading global organisations to equip their managers with the skills, understanding and acumen needed to be financially fit and ready for the challenges of running successful businesses.

Or contact us, to see how we can help you and your organisation…

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

{kind=link}