Welcome to WordPress. This is your first post. Edit or delete it, then start writing!

Finance for Non-Financial Managers: An Introduction to the Balance Sheet

A short guide to the Balance Sheet for Non-Financial Managers…

The Balance Sheet lists a company’s assets and liabilities. It is prepared at a single point in time – and is valid for only that specific date.

It gives a ‘snapshot’ of a business’ financial situation, and reveals where the company’s financing came from – and how those funds were used to buy the company’s assets.

This funding is also referred to as ‘Capital Employed’. Capital Employed comes from three places – profits, loans and shares.

More formally, these sources of finance are known as ‘liability accounts’, organised in terms of equity and loans. This means that on an overall level, Capital Employed equals Equity plus Loans.

As far as the Balance Sheet is concerned, money coming into the business is spent on a combination of Fixed Assets and Current Assets.

A Balance Sheet must always be ‘balanced’. This means that on the date it was put together, the business’ total assets must equal its total liabilities.

On a traditional Balance Sheet, assets and liabilities are kept totally separate from each other.

The ‘working capital’ approach to formatting the Balance Sheet offsets current liabilities against current assets, in order to separately identify working capital.

For many businesses, it helps to separate-out how the business is operated, from how it is financed. So the third way to approach laying-out the Balance Sheet is to use the ‘financial analysis’ format.

This approach clusters all account items relating to company finance on the capital side of the Balance Sheet.

From a financial perspective, a company’s performance is assessed both before and after financing. A number of ratios are used in both situations. Using the financial analysis format for the Balance Sheet makes them easier to calculate.

The figure on the Balance Sheet for Retained Profit is calculated by taking the Retained Profit figure from the P&L and adding it to profits retained from previous financial periods.

This then allows us to calculate the following: Retained Profit from P&L + Retained Profits from previous years + Share capital = Owners’ equity/Shareholders’ funds.

About Brightbolts…

Brightbolts supports business by raising the financial literacy and business acumen of managers.

Brightbolts are specialists in helping managers and organisations raise their levels of financial literacy and commercial awareness. Our suite of customisable Finance for Non-Financial Managers eLearning courses are used by leading global organisations to equip their managers with the skills, understanding and acumen needed to be financially fit and ready for the challenges of running successful businesses.

- View our library of Finance for Non-Financial Managers eLearning courses.

- Have a play with our interactive Balance Sheet widget.

- Take a demo of a customised version of our Finance for Non-Financial Managers eLearning courses.

- Download our Profit Margin Takeaway Infographic.

Or contact us, to see how we can help you and your organisation…

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

Everybody, Somebody, Anybody and Nobody – an animated short from Brightbolts.

Taking ownership is a key part of our philosophy at Brightbolts, we pride ourselves on taking personal responsibility for all our clients, projects, products and programmes. The short story of Everybody, Somebody, Anybody and Nobody therefore really resonated with us, so we thought we would animate it and share it with you all.

Enjoy!

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

Finance for Non-Financial Managers: An Introduction to the Profit and Loss Account (P&L)

A short guide to the Profit and Loss Account (P&L) for Non-Financial Managers…

A short guide to the Profit and Loss Account (P&L) for Non-Financial Managers…

The P&L (also known as the Income Statement) is a Financial Statement that records the level of profit – or loss – that a business earns over a defined period of time (usually one year).

It does this by relating the income (also known as ‘sales’ or ‘revenues’) the business has earned to the costs and expenses the business has incurred.

The P&L starts by recording the income a company has generated through its sales over a given period. It then deducts a series of costs and expenses from this total to determine several different profit measures.

Cost of Sales is deducted from Sales to produce Gross Profit. ‘Cost of Sales’ are those outgoings which are most closely linked with providing services to clients, buying goods for re-sale, or manufacturing products.

Expenses are deducted from Gross Profit to produce Operating Profit or EBIT (Earnings Before Interest and Tax). ‘Expenses’ are incurred in the course of running the business on a day-to-day basis (e.g. advertising costs). They are not directly linked to sales.

Tax on profits and interest on borrowings are deducted from Operating Profit to produce Net Profit After Tax (or NPAT).

Dividends owed to the business’ shareholders are taken away from NPAT, resulting in Retained Profit.

Retained Profit is the proportion of sales/income that the company keeps, and can then use to drive further growth and investment. In this way, it is the ‘wealth’ the company has produced.

Sales may be made – and inputs may be supplied – on credit. This means that cash transactions for both sales and costs may not happen during the financial period.

So measuring profits requires accountants to analyse a company’s operating performance over a given period, by calculating costs incurred and sales made. This must be done accurately, despite the fact that associated cash flows may occur in different time periods.

Costs can only be entered onto the P&L if they relate to business activities that occurred during the period in question.

Materials are only counted if they were ‘consumed’ (otherwise they are counted as ‘stock’ – which is an asset, not a cost).

Services and overheads (e.g. power) are counted when bought (irrespective of cash flows).

Companies will pay interest on short-term bank loans and long-term financing from a variety of sources. Businesses will also receive interest payments on any investments they hold, plus their bank accounts.

The amount of tax owed on a business’ profits is calculated after interest has been deducted. Actual tax paid may be deferred into the future – but what is called a ‘provision’ is made in the P&L at this point to cover that payment, and counted as a deduction.

The level of dividends paid is decided by the business’ Directors. They will consider both the company’s projected cash needs, and what shareholders expect.

Profit & Loss Account – Costs

A business works out how much material it has actually used over the course of a given financial period with the following equation:

Opening stock + Purchases – Closing stock = Materials used.

Usually, materials are valued on the basis of ‘historical cost’ (e.g. what the company paid for them at time of purchase).

Unlike some materials costs, labour costs represent an immediate cash flow out of a company. Most businesses account differently for direct labour costs (e.g. people directly involved in producing a product) and indirect labour costs.

Unlike some materials costs, labour costs represent an immediate cash flow out of a company. Most businesses account differently for direct labour costs (e.g. people directly involved in producing a product) and indirect labour costs.

Depreciation is an accounting method used to spread the cost of capital assets in use for the long-term over the expected length of their ‘useful lifetime’. A depreciation expense is thus charged to the P&L for every year of that ‘asset lifetime’. So if machine costs 100 and is expected to last for 10 years, an annual depreciation charge of 10 (for example) could be charged for every year.

Depreciation is an accounting method used to spread the cost of capital assets in use for the long-term over the expected length of their ‘useful lifetime’. A depreciation expense is thus charged to the P&L for every year of that ‘asset lifetime’. So if machine costs 100 and is expected to last for 10 years, an annual depreciation charge of 10 (for example) could be charged for every year.

There are different ways of classifying the remaining costs that must be accounted for on a P&L. Most companies divide these according to business function e.g. admin, R&D, manufacturing, sales or advertising.

There are different ways of classifying the remaining costs that must be accounted for on a P&L. Most companies divide these according to business function e.g. admin, R&D, manufacturing, sales or advertising.

Including a cost in the P&L is based on whether it has been consumed during the period in question – irrespective of any cash flows out of the company. But this works the other way too: so if something has been paid for in advance, it will not be accounted for on the P&L until the financial period during which it is used.

Sometimes a business will use things that it hasn’t yet been charged for. In such situations (e.g. water used but not yet billed for) the company must make an estimate of the cost, and include that on the P&L.

Some potential (but likely) costs may need to be accounted for on the P&L in the form of provisions: but for these costs, the full details are not yet clear. For example, an on-going court case may result in a future financial liability (e.g. a fine). Here, the exercise of judgement is crucial on a ‘prudent’ basis (e.g. the business should recognise such issues as soon as they become likely).

A business will spend money on some costs (e.g. training) which can properly be counted as ‘intangible investments’ that will benefit it in the future. However, prudence dictates that their costs should still be recognised in the period in which they are incurred.

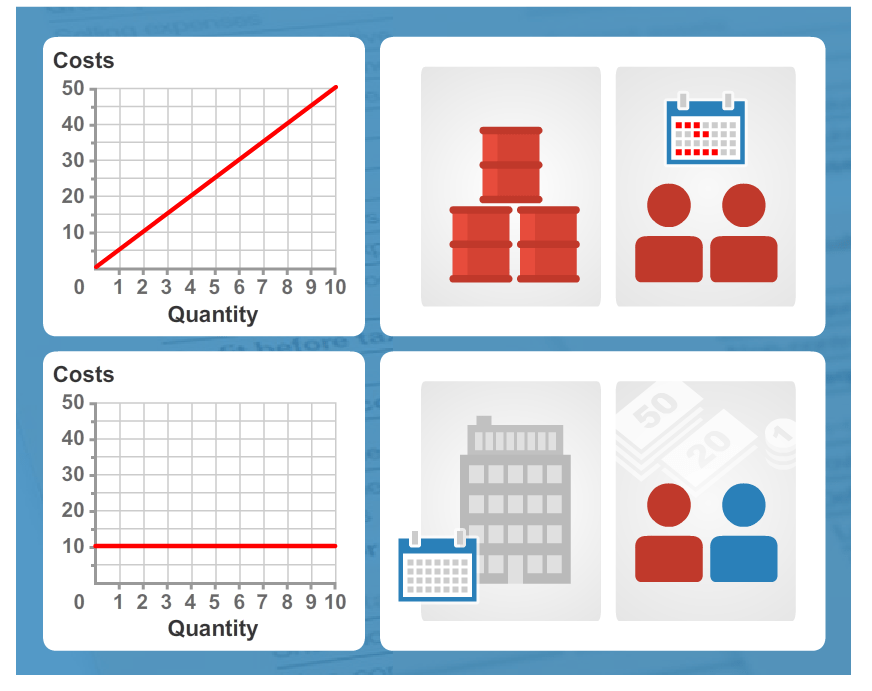

Variable costs are those costs and expenses which change in direct proportion to the level of output (or other business activities). Examples of variable costs include: Temporary labour and materials required to manufacture products; Buying goods for resale; Some selling and admin costs.

Fixed costs are those costs and expenses that usually stay at the same level whatever the level of business activity is (at least over the short term). Examples of these types of costs include office rent and regular salaries.

Breaking down costs into fixed and variable elements allows businesses to identify the marginal costs involved with making extra goods and products more clearly. This is known as ‘variable costing’.

About Brightbolts…

Brightbolts supports business by raising the financial literacy and business acumen of managers.

Brightbolts are specialists in helping managers and organisations raise their levels of financial literacy and commercial awareness. Our suite of customisable Finance for Non-Financial Managers eLearning courses are used by leading global organisations to equip their managers with the skills, understanding and acumen needed to be financially fit and ready for the challenges of running successful businesses.

- View our library of Finance for Non-Financial Managers eLearning courses.

- Have a play with our interactive Profit and Loss Account widget.

- Take a demo of a customised version of our Finance for Non-Financial Managers eLearning courses.

- Download our Profit Margin Takeaway Infographic.

Or contact us, to see how we can help you and your organisation…

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

Finance for Non-Financial Managers: An Introduction to the Financial Statements

A short guide to the Financial Statements for Non-Financial Managers…

The separation of ownership and control for modern businesses means that managers need to make detailed reports to the owners – in the form of Financial Statements.

The question of how well (or badly) a business is doing is answered in the form of the Profit and Loss Account (P&L). The P&L compares a business’ costs and expenses to its sales and works out the difference (e.g. the profits). Also known as the Income Statement, this is a key measure of success (or failure).

The question of how well (or badly) a business is doing is answered in the form of the Profit and Loss Account (P&L). The P&L compares a business’ costs and expenses to its sales and works out the difference (e.g. the profits). Also known as the Income Statement, this is a key measure of success (or failure).

What have managers bought during the period in question? And what obligations have they incurred (aside from the investment funds provided by the owners)? The Balance Sheet provides the answers to these questions. It records: Assets that have been bought; Liabilities that have been incurred; The level of shareholders’ investment funds that have been provided to the business.

What have managers bought during the period in question? And what obligations have they incurred (aside from the investment funds provided by the owners)? The Balance Sheet provides the answers to these questions. It records: Assets that have been bought; Liabilities that have been incurred; The level of shareholders’ investment funds that have been provided to the business.

The Cash Flow Statement is used to record the impact of managers on the changes in a business’ cash holdings over the accounting period, in terms of receipts and payments. The Cash Flow Statement details this by analysing changes in key items on the Balance Sheet, and the extent to which cash flow has been generated from profits.

Financial accountants’ are guided in their efforts to provide consistent financial information to the owners of a business by what are called ‘accounting standards’. These standards vary in different countries. Auditors (another kind of accountant) then check the resulting Financial Statements against these same standards.

Financial accountants’ are guided in their efforts to provide consistent financial information to the owners of a business by what are called ‘accounting standards’. These standards vary in different countries. Auditors (another kind of accountant) then check the resulting Financial Statements against these same standards.

Management accountants work with the same data that is used by financial accountants – but their reports are used for internal purposes. ‘Management accounting’ produces very detailed information that the managers of the business use to help them make future decisions (e.g. investment choices) – and thus contributes to the overall results of the business over time.

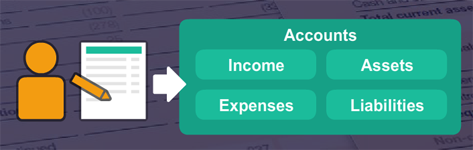

Every transaction a business makes is classified according to its nature, and recorded via the creation of two corresponding entries in one or two of these four types of account: Income; Expenses; Assets; Liabilities.

The Income Accounts of a business are used to record all of the income that it has earned, from a variety of sources. These include: Interest payments received (or due); Sales of services or products.

A business’ Expense Accounts record costs of all types, such as: General expenses required to run a business and sell its products and services; Specific costs of making, buying or preparing products and/or services that are then sold; Interest that has been charged on any funds it has borrowed.

The Asset Accounts of a company record all of the assets that are either currently owned by that business, or which are owed to it. There are two key types of asset – Fixed Assets and Current Assets.

The Liability Accounts of a business will record two things: Any ‘monies’ for which the company is liable (based on past transactions); Where the funds have come from that are being used in the business.

Liability accounts break down into three main types: Equity (e.g. the funds provided by the owners of the business); Loans (e.g. all of the funds that the business has borrowed in the past); Creditors (e.g. the money that the company owes for the things that it has bought).

Liability accounts break down into three main types: Equity (e.g. the funds provided by the owners of the business); Loans (e.g. all of the funds that the business has borrowed in the past); Creditors (e.g. the money that the company owes for the things that it has bought).

About Brightbolts…

Brightbolts supports business by raising the financial literacy and business acumen of managers.

Brightbolts are specialists in helping managers and organisations raise their levels of financial literacy and commercial awareness. Our suite of customisable Finance for Non-Financial Managers eLearning courses are used by leading global organisations to equip their managers with the skills, understanding and acumen needed to be financially fit and ready for the challenges of running successful businesses.

- View our library of Finance for Non-Financial Managers eLearning courses.

- Take a demo of a customised version of our Finance for Non-Financial Managers eLearning courses.

- Download our Profit Margin Takeaway Infographic.

- Have a play with our interactive Profit Margin widget.

Or contact us, to see how we can help you and your organisation…

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

Do serious business people play games?

Gamification

The profile of gamification is growing within the eLearning industry, with dedicated conferences, books and detailed research being published by experts. More and more organisations are also starting to experiment with gamification techniques. However, there are issues with effectiveness, clearly demonstrated by the quote from Gartner who say that 80% of current gamified applications fail to meet the set business objectives, primarily due to bad design.

So what exactly is gamification?

There is no single definition for gamification. However, in the context of eLearning, it essentially is the use of gaming elements and game design to increase the effectiveness of the learning. Adding value to the experience through the use of gaming elements such as:

- Point scoring and badges

- Leader boards

- Competitive elements and challenges

- Levels and progression

- Rewards and punishment

- Avatars

Is the concept driven by demand or is it a concept that the industry is prescribing?

The jury is out on this one. The first academic papers and research came about in the 1980s and since then many organisations have come and gone who focused on the serious application of games.

An interesting clue as how to perhaps answer the above question can be taken from the below statistics.

- The gaming industry is currently worth $57 billion

- The average gaming consumer is 30 years old

- The gender divide is 55% male 45% female

Providing it is done well, gamification should then have the potential to be a powerful and popular technique. Making the mundane a little more fun and providing a safe environment to make creative and innovative solutions to modern business problems.

Successful gamification

The keys to success with gamification are:

- Don’t use it for the sake of using it

- Set a clear objective that the game is to achieve

- The game needs to effectively transfer learning

- It needs to be right for the audience and demographic you are trying to teach

- The game needs to motivate the learner and add extra interest

- It’s purpose should be meaningful

- The game should provide a platform to make autonomous decisions

- It should provide a pathway to allow the individual to improve

- It should be designed well

- The relevant stakeholders should be involved at every step of the process

At Brightbolts we specialise in creative and effective eLearning solutions. Whether it be a simple TakeAway learning infographic, a Snippet of mobile learning or a full-on Chunk of eLearning, we will provide the solution that best meets your needs.

Please contact us for a chat about your requirement and to find out how we can best help…

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

We are ELEARNING SUPERSTARS…

A module from our Finance for Non-Financial Managers elearning courses has been picked up and positively reviewed by Elearning Superstars.

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

A visual history of human knowledge

In this fascinating TED presentation, infographics expert Manuel Lima explores the thousand-year history of visualising information and explains the increasing shift away from using knowledge trees to networks of information.

At Brightbolts, we love an infographic. Our beautiful, clear and simple TakeAway learning infographics are designed for the immediate consumption and digestion of your complex information:

- Present complex information quickly and clearly

- Improve cognition by tapping into the human visual system

- Designed to be viewed on all devices

- Can be scaled to any size for printing as posters

- Can be static, animated and interactive

Download an example of one of our TakeAway Infographics here and contact us to see how we can help you visualise your information either as part of an eLearning programme or as a stand-alone solution.

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

Why do so many small businesses fail in their first year?

There is no doubt that the environment for business is tough, with 50% of small business expected to fail within 5 years. Many of the adverse factors affecting business, such as tax and bank lending are out of the operational control of business owners and managers. So in order to survive, small business needs to make the most of their resources and ensure that they have the knowledge and skills to survive.

Also listed among the common reasons for the failure of small business are:

- A lack of business acumen,

- Poor financial planning,

- Bad cash flow management.

To survive, business owners and managers of small enterprises must be able to rise above the minutia of day-today business decisions and see the bigger picture.

They must understand how the cogs of business fit together to impact profitability and cash flow, and they must be able to assess the impact of their potential decisions on the success of the business.

To truly understand the business, owners and managers have to understand how their business makes money – in other words, how it generates sales, maximises profit and manages cash. They need to understand that every action taken and every decision in each area of their business will impact these ultimate measures of business success.

Business owners and managers of small enterprises are typically forced to develop this business acumen on their own. They are hands-on with their businesses, having to make all the decisions as they go along, whether good or bad. As the statistics show, they either learn from their mistakes or fail.

Common problems for SMEs

Small and Medium Enterprises (SMEs) are often confronted with problems that are uncommon to the larger companies and multi-national corporations. These problems include the following:

- Lack of Credit: SMEs frequently have difficulties in obtaining capital or credit, particularly in the early start-up phase.

- Profit vs Cash: Understanding the difference between profit and cash.

- Cash Flow Management: Protecting and enhancing their cash flow position.

- Financial Statements: Understanding financial statements and their use in making better business decisions.

- Survival, stabilisation and planning for the future.

- Working capital, investments, financing business assets or assistance with international trade.

- Restricted Resources:Their restricted resources may also reduce access to new technologies or innovation.

- Resistance to Change: Many of the employees in SMEs started from the ground up after working with the company for many years. Some of them are often holding supervisory and managerial positions. These employees may not be IT literate and often have high resistance to the changes in the working process that they are comfortable with after many years.

- Lack of Procedure: Most SMEs do not have formal procedure or often these are not documented. Furthermore, there is tendency for these procedures to change frequently. This makes it difficult for third parties and newcomers to understand the existing business practices.

- Lack of Managerial Training and Experience: Managers who are promoted from the rank and file may not have had the exposure or training needed to perform as leaders and managers of people.

- Manpower: SMEs are frequently fire fighting and suffer from shortage of manpower.

Brightbolts supports business by raising the financial literacy and business acumen of managers.

Brightbolts are specialists in helping managers and organisations raise their levels of financial literacy and commercial awareness. Our suite of customisable Finance for Non-Financial Managers eLearning courses are used by leading global organisations to equip their managers with the skills, understanding and acumen needed to be financially fit and ready for the challenges of running successful businesses.

- View our library of Finance for Non-Financial Managers eLearning courses.

- Take a demo of a customised version of our Finance for Non-Financial Managers eLearning courses.

- Download our Profit Margin Takeaway Infographic.

- Have a play with our interactive Profit Margin widget.

Or contact us, to see how we can help you and your organisation…

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]

How financially fit are your managers?

{kind=link}

Most people in management, start their careers as specialists and high-achievers from within the business. Their potential is obvious, so they are promoted through the ranks. But, being an amazing and innovative engineer or a big-hitting sales person does not mean that you will naturally be a great leader.

Many career paths just do not provide the necessary exposure to managing people, budgets and to understanding the nuts and bolts of business that are essential to becoming a successful manager.

From the outset, managers are expected to be decision makers and leaders, this is a heavy burden to carry when you do not have the necessary commercial awareness to understand the full implications of the decisions that you are making.

Becoming financially literate and commercially aware should be one of the first development needs addressed by all managers.

Managers need to understand how a business makes its money, manages its cash, maximises its profits and how each person, role and function can positively influence business performance.

Managers need to own a fundamental foundation of financial literacy, or an understanding of the financial statements and an operational understanding of how they can best use this financial information to make decisions that positively impact on the success of the business.

Being commercially aware is the difference between being able to read and understand financial statements and being able to read, understand and interpret this information to make informed business decisions.

When commercial awareness is embedded in an organisation, its managers begin to ask more informed questions.

Questions that take into account the impact of potential decisions on different parts of the business and also how the outcome of their decisions will finally impact upon the company’s financial performance and results.

- Has the cost of production gone up? If so, why?

- Have we changed our pricing model? If so, how has that affected our margins?

- If our production unit costs have gone up, can we better control our production processes or service delivery?

- Is there a way to produce a greater product volume at the same cost?

- Can we raise prices, yet still provide value to the customer and remain competitive?

- Are we creating value for our shareholders?

When questions become more informed, the right decisions can be made.

Brightbolts are specialists in helping managers and organisations raise their levels of financial literacy and commercial awareness. Our suite of customisable Finance for Non-Financial Managers eLearning courses are used by leading global organisations to equip their managers with the skills, understanding and acumen needed to be financially fit and ready for the challenges of running successful businesses.

- View our library of Finance for Non-Financial Managers eLearning courses.

- Take a demo of a customised version of our Finance for Non-Financial Managers eLearning courses.

- Download our Profit Margin Takeaway Infographic.

- Have a play with our interactive Profit Margin widget.

Or contact us, to see how we can help you and your organisation….

[share title=”Share this Post” facebook=”true” twitter=”true” google_plus=”true” linkedin=”true” style=”color:#000″]